18 / 94

18 / 94

Step

1

Identification

Context

Prioritization

Materiality

Review

Validation

Completeness

Step

2

Step

3

Step

4

Sustainability Context

Stakeholder Inclusiveness

Stakeholder Inclusiveness

Reporting

18

(G4-19)

SET started disclosing operational results and direction for sustainability development in 2012, via its

“Social

Responsibility Report”

annual publication. In 2013, the report was re-named as the

“SET Sustainability Report”

,

in line with internationally accepted Global Reporting Initiative (GRI) G3.1. Since then, SET has been developing an

accurate and complete reporting process according to international standards, to keep stakeholders updated about

SET’s development and performance. This report discloses SET’s sustainability operating results during January 1

– December 31, 2015, available on SET’s website

3

and in hard copy.

Reporting approach

The 2015 SET Sustainability Report is “in accordance”

with the Core option of the GRI G4 Guidelines.

Data collection

The data collection for this year’s Sustainability Report

was carried out by using two methodologies: qualitative

and quantitative. The qualitative data collection was

conducted by interviewing related parties and SET

employees who have directly and indirectly contacted

the stakeholders. The quantitative data was obtained

from reliable sources with standard calculation formulas.

The processed data and information were then gathered,

summarized and drafted in a report format before sending

back to the interviewee’s organization and data owner

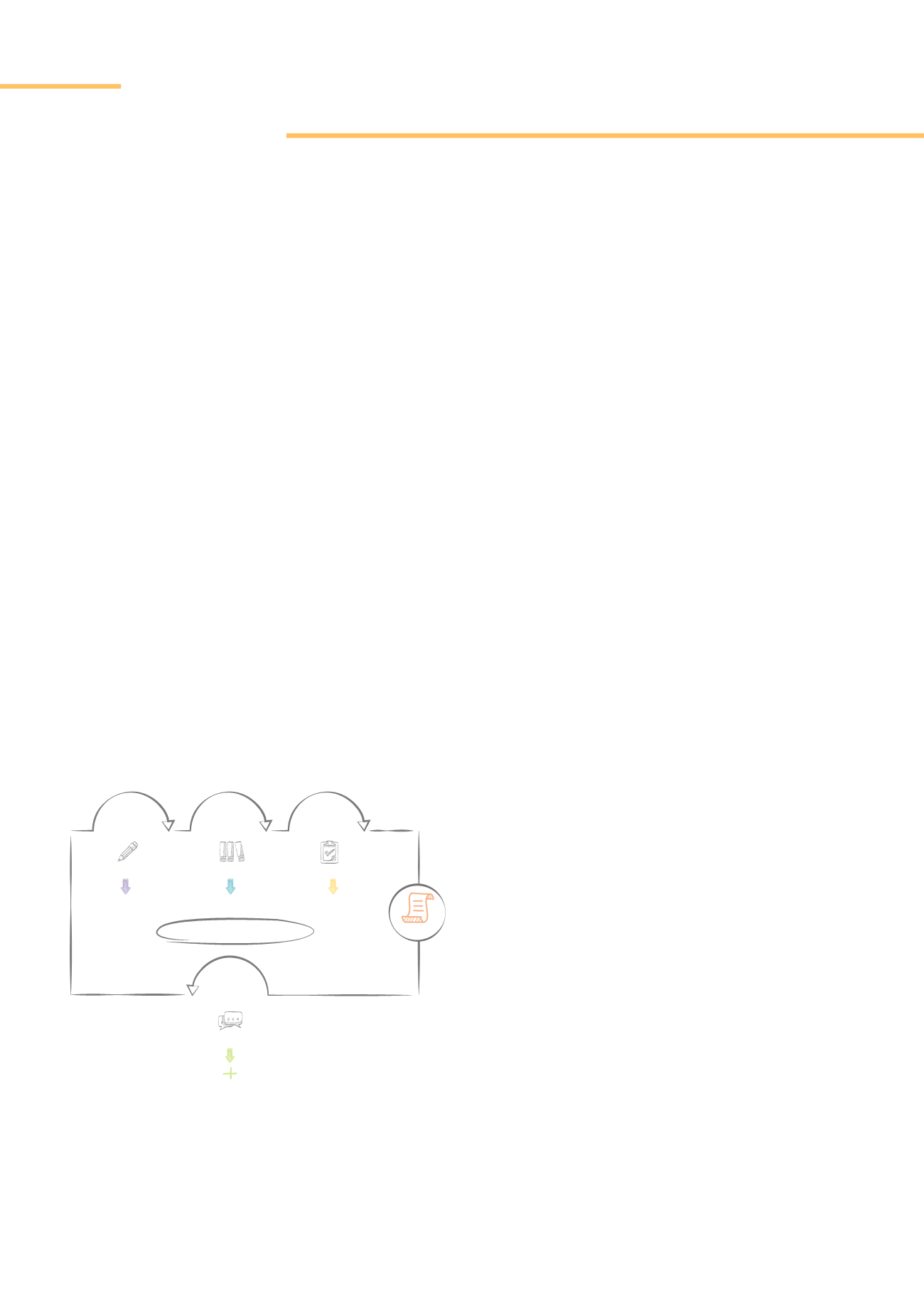

for review. The report contains four steps: identifying

materiality, prioritizing, checking accuracy and reviewing

key issues.

Scope of the report

SET determines the scope of report to be in line with

operational results based on sustainability context and

stakeholder inclusiveness. SET’s sustainability framework

covers five areas: Market growth, Sustainability management,

Employees, Social concerns, and Environmental concerns,

as demonstrated in this report.

Material aspects

As the sustainability framework in five areas has covered

the context and links to all stakeholders, then materiality

analysis has to be conducted make the report concise

and clear. The materiality analysis results are as follows:

1. The development of all stakeholders in the

capital market must take environmental, social

and governance (ESG) performance into

consideration

2. Sustainable and performance-driven management

3. Being the employer of choice

4. Social impact investment

5. Building financial literacy

6. Implementation of policy on natural resources

and environment or “Green policy”

About

the Report

3

www.set.or.th/th/about/annual/sd_report_p1.html(G4-18)